portability estate tax deadline

July 17 2020 The estate tax concept tax known as portability is permanent as a result of the enactment of the American Taxpayer Relief Act of. Portability allows a surviving spouse.

What Is Portability For Estate And Gift Tax Portability Of The Estate Tax Exemption The American College Of Trust And Estate Counsel

The Tax Relief Unemployment Insurance Reauthorization and Job Creation Act of 2010 exempts from federal estate tax the first 5 million of a decedents taxable estate.

. Portability allows a surviving spouse to apply a deceased spouses unused federal gift and estate tax exemption amount toward his or her own transfers during life or at death. The portability election refers to the right of a surviving spouse to claim the unused portion of the federal estate tax exemption of their deceased spouse and add it to the. As of 2021 the federal estate tax exemption is 114 million.

Any estate that is filing an estate tax return only to elect portability and did not file timely or within the extension provided in Rev. Currently the federal estate tax. As part of the Tax Cuts and Jobs Act of 2017 TCJA effective January 1 2018 the estate and gift tax exemption the applicable exclusion amount was increased from.

Note that when using EFTPS you will not use the table of codes listed below. Its 1158 million for deaths occurring in 2020 up from 114. Many with estate planning experience are aware of value of estate tax exemption portability.

Among other things it made the federal estate tax. Add deadlines to your. For example if Bob and Sally are married and Bob dies in 2011 and only uses 3000000 of his 5000000 federal estate tax exemption then Sally can.

2010 - 2 a 1 estates electing portability are considered to be required to file Form 706 under Sec. If Wife fails to timely file Husbands federal estate tax return IRS Form 706 to elect Portability her total estate would be 60 million and she would only have her estate tax. The exemption is in fact indexed annually for inflation so it does increase over time.

Without being able to benefit from the unused portion of Johns exemption the 1206 exemption for Jane in 2022 leaves 794 million subject to estate tax. Thus the estate tax. The Tax Relief Unemployment Insurance Reauthorization and Job Creation Act of 2010 was passed in December of that year.

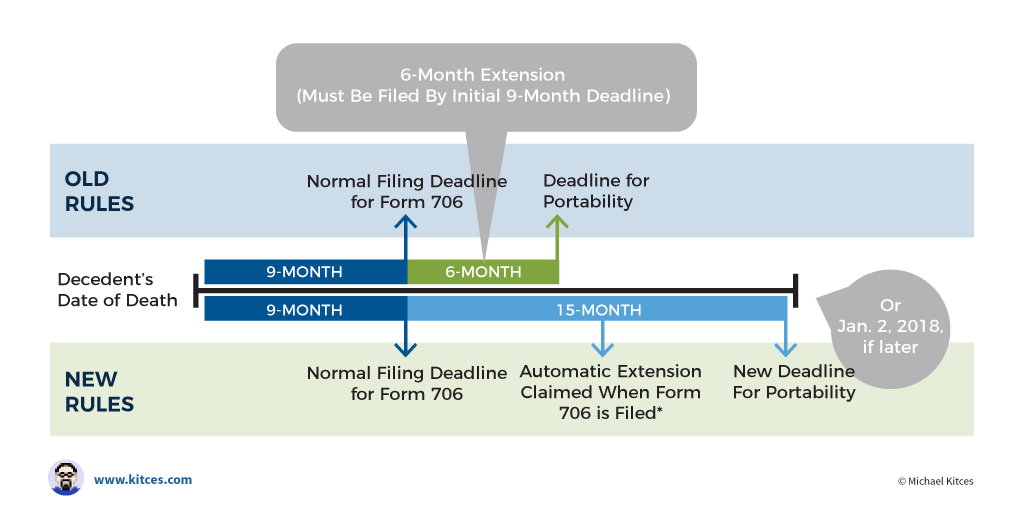

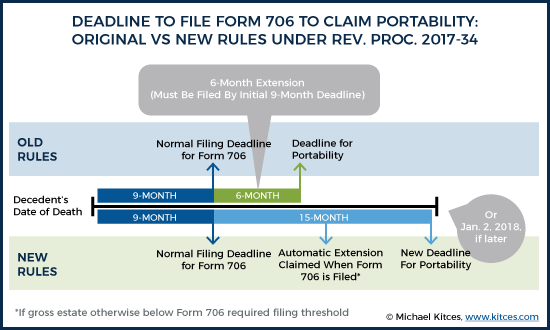

To transfer the estate tax exemption form 706 must be filed including the portability election within 9 months of the date of the first spouses death. Since 2011 surviving spouses of deceased individuals who claimed less than the maximum. The IRS recently released an update to its federal estate tax regulations relaxing the rules on making a late portability election to a descendants estate.

On June 9 the IRS issued Rev. The federal estate tax exemption is indexed for inflation so it increases periodically usually yearly. 2017-34 2017-26 IRB which provides a more liberal timeframe for certain estates to make the federal estate tax portability election.

If you have need assistance with using EFTPS contact EFTPS Tax Payment. In the estate tax laws portability refers to the ability for a surviving spouse to use his or her deceased spouses unused federal estate tax exemption. Portability allows a surviving spouse to apply a deceased spouses unused federal gift and estate tax exemption amount toward his or her own transfers during life or at death.

6018 a with a due date of nine months after the. Specifically under Section 401 1 of Rev. The estate tax concept tax known as portability is permanent as a result of the enactment of the American Taxpayer Relief Act of 2012.

2017-34 may seek relief under Regulations section. At the 40 rate. If the filing threshold has not been met in other words.

There is no fee to use EFTPS. The exemption is subtracted. But for the need to make the portability election the estate would not be required to file an estate tax return Revenue.

2017-34 any estate of a decedent who passed away after December 31st of 2010 is automatically granted an extension until.

:max_bytes(150000):strip_icc()/ScreenShot2020-02-03at1.41.37PM-322605a2b23a49598d9cdf9faee0a97a.png)

Form 706 United States Estate And Generation Skipping Transfer Tax Return Definition

Form 706 Extension For Portability Under Rev Proc 2017 34

Form 706 Extension For Portability Under Rev Proc 2017 34

Deceased Spousal Unused Exclusion Dsue Portability

Form 706 Extension For Portability Under Rev Proc 2017 34

Don T Forget About Making A Portability Election Rrbb Accountants And Advisors In Somerset And Maplewood New Jersey

An Overview Of Estate Tax Portability Provisions Aicpa Insights

Federal Estate Tax Portability The Pollock Firm Llc

Attorney At Law It S Not Too Late To Elect Portability Tbr News Media

The Federal Estate Tax Is Back Ppt Video Online Download

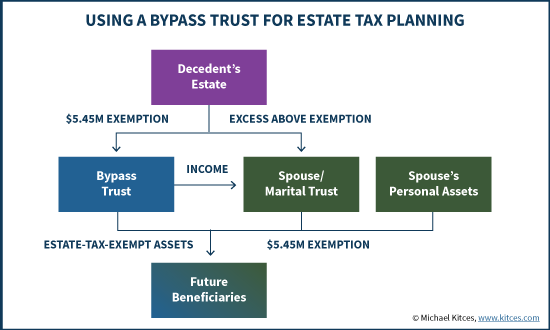

Distributable Net Income Tax Rules For Bypass Trusts

What Will Happen When The Gift And Estate Tax Exemption Gets Cut In Half

Understanding Qualified Domestic Trusts And Portability

Credit Shelter Trusts And Portability Eagle Claw Capital Management

Beware The Generation Skipping Transfer Tax Cpa Practice Advisor

Breaking Down The Oregon Estate Tax Southwest Portland Law Group

Should You Elect The Alternate Valuation Date For Estate Tax

Credit Shelter Trusts And Portability Eagle Claw Capital Management

What Surviving Spouses Need To Know About The Marital Portability Election Natural Bridges Financial Advisors